World Economic Prospects

Each month Oxford Economics’ team of 450 economists updates our baseline forecast for 200 countries using our Global Economic Model, the only fully integrated economic forecasting framework of its kind. Below is a summary of our analysis on the latest economic developments, and headline forecasts. To access the full report (and much more), request a free trial today.

Request a free trial

Economic consequences of the Middle East conflict will linger beyond any truce

- We’ve lowered our world GDP growth forecast by 0.4ppts since the start of March to 2.4% because we expect a more prolonged disruption to shipping activity through the Strait of Hormuz. The fragile ceasefire seemingly reduces the risk of a far worse outcome. But even if a truce is maintained, it will take time for energy production and shipping traffic to return to normal levels.

- We assume that the Strait of Hormuz will remain effectively closed until the end of April. Traffic levels then rise to around 50% in May and June, before gradually recovering to normality over the following six months. This results in the Brent oil price averaging around US$113 per barrel in Q2 before falling to just under US$80pb by the end of this year, in line with the assumptions in our second forecast release in late March.

- The higher oil price along with increases to our gas, fertiliser, and agricultural commodity price forecasts are expected to push world CPI inflation up to a peak of 4.4% in Q2. While this is an unwelcome development for households and policymakers, this would be around half the peak inflation rate recorded in 2022.

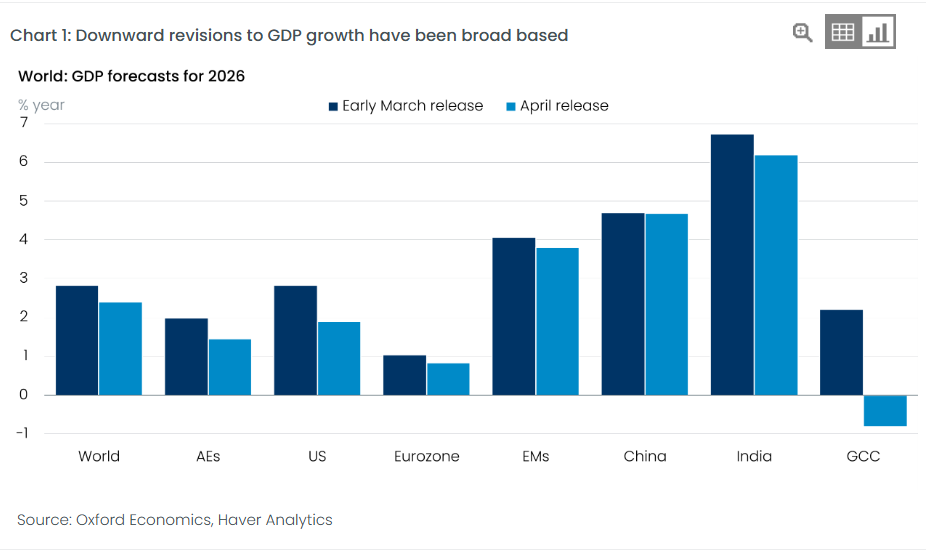

- Downward revisions to GDP growth in 2026 have been broad-based, reflecting heightened uncertainty, the squeeze to household real incomes, and disruption from energy shortages, particularly in Asia. The US downgrade from 2.8% to 1.9% is due to weaker-than-anticipated activity at the start of this year.

- Central banks face an uncomfortable choice– hike rates and worsen the economic outlook, or risk an increase in inflation expectations. We expect the ECB’s hawkish bias and the low starting point for policy rates to prompt two hikes of 25bps. By contrast, we still expect the Federal Reserve to lower rates by 25bps in June and September. Overall, we expect central banks to behave less hawkishly than markets anticipate.

Request a Free Trial

Complete the form below and we will contact you to set up your free trial. Please note that trials are only available for qualified users.

We are committed to protecting your right to privacy and ensuring the privacy and security of your personal information. We will not share your personal information with other individuals or organisations without your permission.

Find out how Oxford Economics can help you

Talk to us