Bridging the Gap: How our CECL and IFRS 9 scenarios support with US stress testing

Earlier this year, the Federal Reserve Board published its 2026 Comprehensive Capital Analysis and Review (CCAR), outlining the latest annual stress test for large US banks.

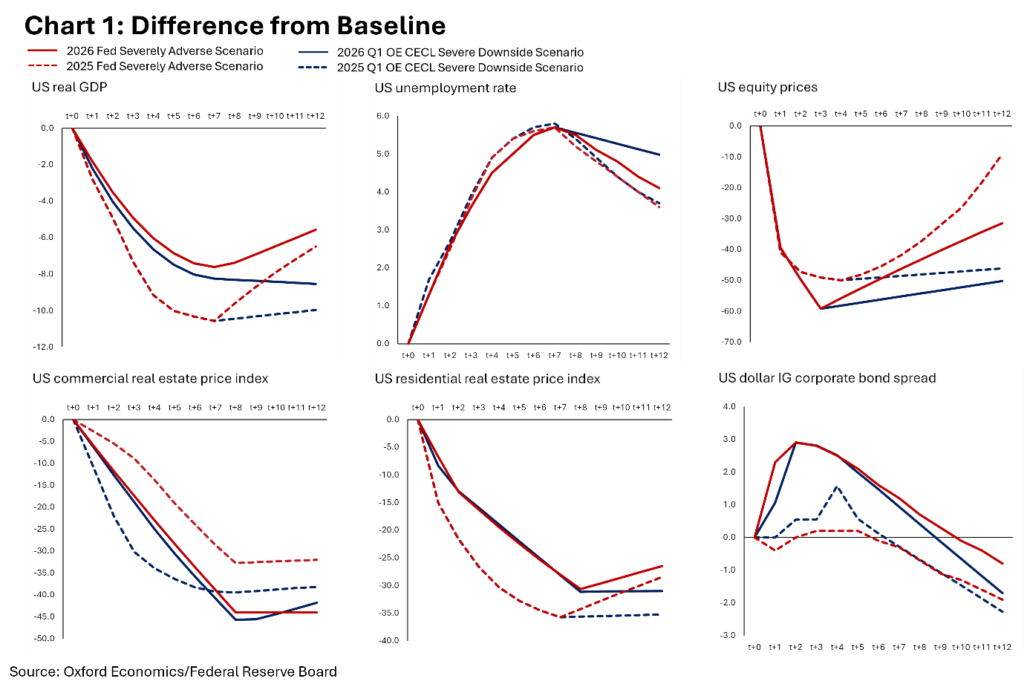

The 2026 severely adverse scenario introduces a more structured and transparent design, with a greater reliance on a published macroeconomic model to ensure consistency across key variables such as GDP, unemployment and inflation. Although the overall narrative remains broadly similar to previous stress tests, it has been updated to reflect conditions at the time of publication. This includes a refined global market shock component that targets areas of heightened risk, alongside a more explicit treatment of financial market stress.

Compared with the 2025 exercise, the key change lies in how risks are calibrated. Under the new methodology, the downturn in GDP and residential housing is somewhat less pronounced, while pressure on commercial real estate prices, equities and corporate credit spreads are more severe. This reflects both a greater reliance on the macro model to anchor the path of the US economy, new “jump-off” conditions, and continued global uncertainty that increases the importance of macroeconomic risks. As a result, additional stress is applied to financial markets and conditions to capture how these risks may transmit to the wider economy.

To support clients in aligning with the evolving regulatory framework, we translate the Fed’s CCAR guidance into our CECL Severe Downside scenario. Using the Global Economic Model, we expand US-specific paths into a fully consistent global framework, capturing global spillovers and cross-market dynamics.

When comparing the Fed’s updated guidance with our existing methodology for CECL and IFRS 9 scenarios, which are based on our proprietary dataset of 30-years of forecast errors, we find that the scenario projections now align more closely. This is particularly evident in key variables such as GDP and unemployment, where the Fed’s model-driven approach produces trajectories that are broadly consistent with the downside tail of our forecast distributions.

Benchmarking the Fed’s severely adverse scenario against our distribution-based framework shows that it broadly aligns with (and in some cases exceeds) our 99th percentile scenario. However, the shape of the stress differs. The Fed’s scenario is more cyclical, with a sharper initial downturn followed by a smaller recovery. By contrast, our scenario reflects both cyclical and structural risks over a longer horizon, capturing hysteresis from severe shocks that result in a lower trend of economic outcomes.

This distinction reflects a broader difference in methodology. The Fed’s model-based framework delivers a consistent, standardised stress outcome at a point in time. Whereas our distribution-based approach is anchored by historical forecast errors, providing a probabilistic view of risk that captures both the severity and likelihood of outcomes. This framework also evolves dynamically with the macroeconomic environment, incorporating changes in the baseline outlook and shifts in the balance of risks through regular updates between Fed CCAR exercises.

As a result, our CECL and IFRS 9 scenarios provide a valuable complement to regulatory stress tests. While the Fed’s severely adverse scenario offers a standardised annual benchmark for extreme outcomes, our approach enables continuous and forward-looking risk assessment. By combining regulatory guidance with a flexible, data-driven framework, lenders can assess resilience under both global shocks and evolving macroeconomic conditions more comprehensively.

Click here to learn more about our IFRS 9 service and here for our CECL service.