How the Iran war is reshaping commodity markets in 2026

By Stephen Hare, Kiran Ahmed, Sebastien Tillett

Commodity markets have shifted sharply in 2026. What was expected to be a relatively balanced year has instead been defined by the Iran war and the resulting geopolitical shock in the Middle East. The effective closure of the Strait of Hormuz has disrupted global supply chains and triggered a broad repricing across energy, metals and agricultural commodities.

In this blog, we explain what is driving the shift, how it is feeding through different markets and what it means for the commodity price outlook in 2026.

A decisive shift in the 2026 commodity outlook

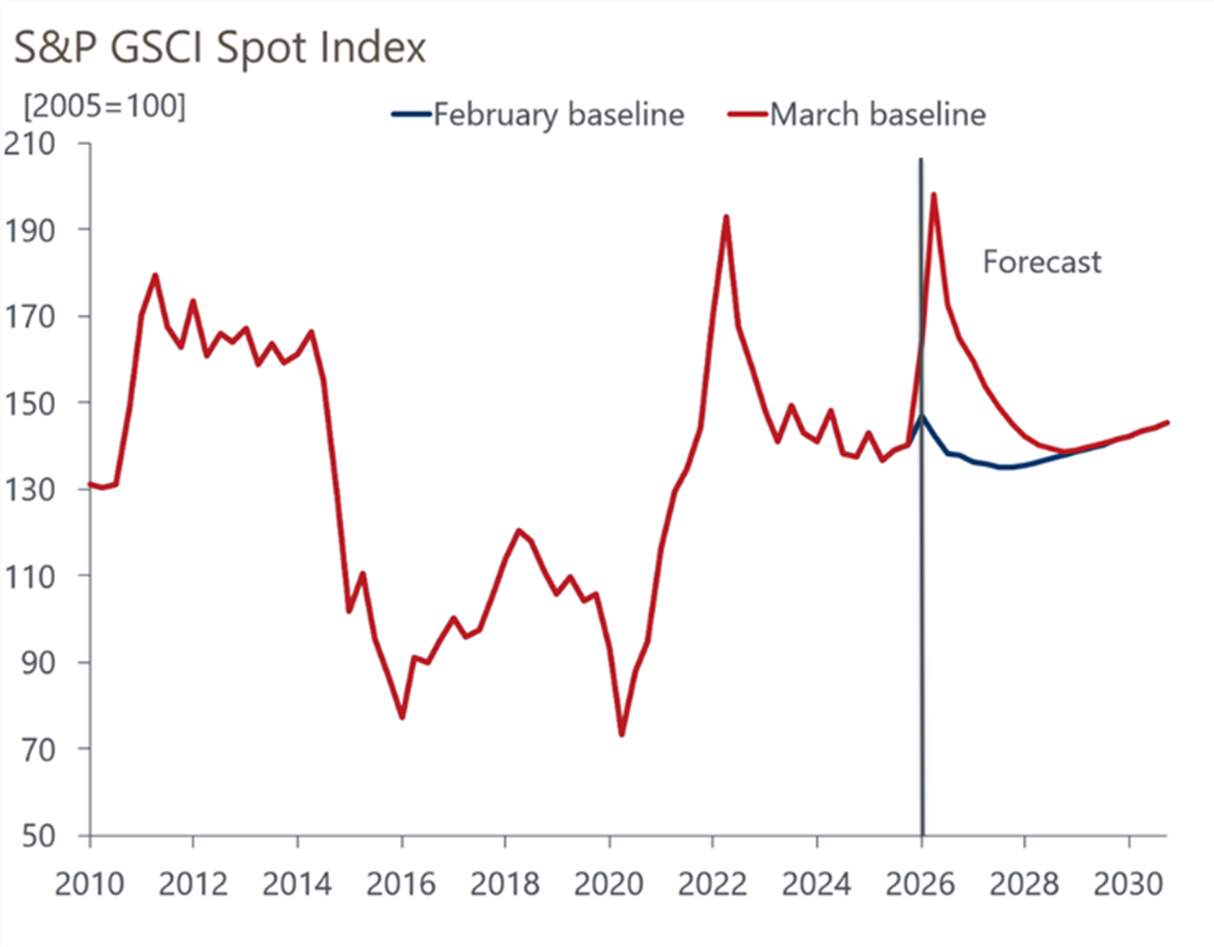

At the start of the year, commodity markets were expected to follow a broadly stable path. Modest demand growth and relatively robust supply, particularly in energy, pointed to weaker prices.

That outlook has now reversed.

Geopolitical disruption has become the dominant driver of price formation. Supply shocks, logistical constraints and precautionary behaviour are now outweighing traditional supply and demand dynamics. More than two thirds of commodities are expected to record price increases in 2026.

The chart shows how sharply expectations have shifted, with the aggregate commodity price outlook revised significantly higher. This marks one of the most significant forecast revisions in recent years, underlining how quickly geopolitical disruption can reprice global commodity markets.

Energy markets at the centre of the Iran war shock

Oil markets tighten rapidly

The Strait of Hormuz is a critical global energy corridor, carrying around one fifth of global oil and LNG trade. Its disruption has removed a major supply channel and sharply tightened market balances.

Around 10 million barrels per day of oil exports have been stranded, with only partial rerouting available. This has pushed Brent crude above $100 per barrel, with prices expected to rise further in the near term.

Even as flows begin to recover, normalisation is likely to be gradual. Restarting production, clearing logistical backlogs and managing ongoing security risks will continue to constrain supply. As a result, a sustained geopolitical risk premium is now embedded in oil prices.

Gas markets under even greater pressure

Natural gas markets have seen an even more pronounced shock. The shutdown of Qatari LNG exports, which account for roughly one fifth of global supply, has driven sharp price increases.

The impact is most severe in Europe and Asia, where reliance on LNG imports is highest. European prices have been revised up significantly due to both supply losses and the need to rebuild storage. By contrast, US prices have risen only modestly due to domestic supply insulation.

This divergence highlights how regional exposure and infrastructure constraints are shaping price outcomes across gas markets.

Industrial metals: A growing divergence

Aluminium leads the upside

Aluminium is the most exposed industrial metal in the current environment. The Gulf region accounts for a meaningful share of global supply, meaning disruptions have an immediate impact on availability.

At the same time, aluminium production is highly energy intensive. Rising energy prices are pushing up production costs globally, reinforcing upward pressure on prices.

Prices are expected to approach $3,450 per tonne in the second quarter, close to record levels.

However, further gains are likely to be capped. Higher prices will weigh on demand, encourage substitution and eventually lead to some moderation later in the year. The balance between supply disruption and demand destruction will be key in determining the path ahead.

Other metals face cyclical pressure

In contrast, other base metals such as copper are facing weaker fundamentals. Recent price strength has been partly driven by speculative positioning rather than underlying demand.

As financial conditions tighten, this support is beginning to unwind. A stronger US dollar and rising inventories are adding further downward pressure.

This creates a clear divergence within the metals complex, with aluminium supported by disruption and costs, while others remain exposed to cyclical weakness and softer demand conditions.

Agriculture commodities: Cost pressures build

The Iran war’s impact is also feeding into agricultural markets.

Fertiliser is a key transmission channel. Around one third of global fertiliser production passes through the Strait of Hormuz, making it highly exposed to disruption. At the same time, higher natural gas prices are raising production costs.

Fertiliser prices are now expected to be nearly 20 percent higher year on year in the second quarter.

This comes at a critical point in the planting season. Higher input costs are likely to reduce fertiliser use and influence crop choices. Farmers may shift towards less fertiliser intensive crops, while higher fuel costs increase transport and machinery expenses.

Global food prices are now forecast to rise by around 6 percent in 2026, with further pressure likely as lower fertiliser use feeds into reduced yields. The full impact is therefore likely to extend beyond 2026 and into subsequent harvest cycles.

Gold: safe haven, but more volatile

Gold has remained supported but is behaving less predictably.

While it is often seen as a safe haven, gold does not always rise immediately during geopolitical shocks. Liquidity pressures can lead to short term declines as investors sell assets to raise cash.

More sustained gains tend to occur when geopolitical stress coincides with looser monetary policy and lower real yields.

Recent price movements reflect this interaction. Gold has been supported by expectations of policy easing but remains volatile as those expectations shift.

Over the medium term, central bank buying and reserve diversification are expected to provide continued support, although short term fluctuations are likely to remain pronounced.

What this means for commodity prices in 2026

Commodity markets in 2026 are being shaped by three interconnected forces:

- Direct supply disruption, particularly in energy

- Cost transmission into metals and agriculture

- Financial amplification through investor behaviour and policy expectations

These dynamics mark a clear shift. Markets are no longer driven primarily by gradual changes in supply and demand, but by discrete shocks and their transmission across sectors. This increases both volatility and cross market linkages.

Final thoughts

While some pressures may ease as supply adjusts, geopolitical risk is likely to remain a key driver of commodity prices in 2026. The effects of the conflict are broad-based, shaping energy, agricultural and financial markets as well as industrial production.

In an environment like this, navigating volatility requires more than monitoring headlines. It requires understanding how these shifts translate into input costs, margins and risk exposure across markets and regions, supported by timely forecasts, scenario analysis and a clear view of how markets are evolving.

Explore our latest commodity forecasts, Iran war analysis, and interactive dashboards, request a trial of our Global Commodity Service today.

You might also be interested in

Subscribe to our newsletters

Sign up to our newsletter to download the latest and most popular reports.

SubscribeAccess our latest commodity forecasts and market insights. Request a trial today.

Subscribe to our newsletters

Sign up to our newsletter to download the latest and most popular reports.

Subscribe