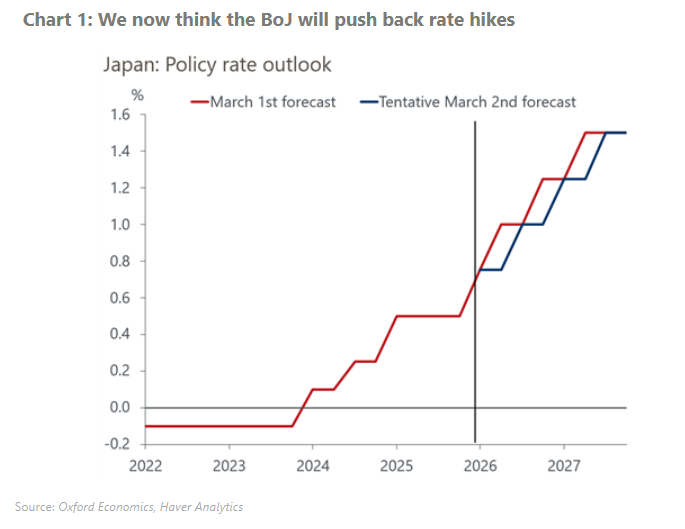

The Bank of Japan (BoJ) kept its policy rate at 0.75% at its March meeting. We now project the central bank will delay the next rate hike to July from June given the economy could fall into stagflation. Thereafter, the bank is projected to continue gradual rate hikes in Q1 and Q3 2027.

Higher energy costs will re-accelerate supply side-driven inflation in the near term. We now think that core-core CPI will return to 2% only in Q2 2027 instead of Q4 2026. Despite the projected robust outcome at the Spring Negotiation, higher inflation will limit real income growth. We’ve therefore lowered our real GDP growth forecast by 0.4ppts to 0.3% in 2026.

In our worst-case scenario, CPI spikes to around 5% y/y in Q2 and stays above 4% throughout 2026, forcing the economy into a mild contraction in 2026. The risk of financial market disruption also rises as, in addition to a fall in equity prices and the yen, rising concerns about fiscal sustainability and higher inflation may put upward pressure on long-term yields.

Despite concerns about pressure on inflation expectations and a weaker yen, we believe that the BoJ will likely become more cautious on rate hikes, instead prioritizing the impacts on corporate profits and real household income. Japan is structurally vulnerable to terms-of-trade shocks.

The recent selection of two new BoJ board members confirmed Prime Minister Sanae Takaichi’s cautious stance on rate normalization. Although the Iran conflict could further enhance her reluctance, we still believe that Takaichi will accept rate hikes if market concerns about the risk of the BoJ falling behind the curve intensify pressures on the yen and long-term yields.